Turning Paper Into Proof: Why We Took Secondaries

By: Mikayla Mooney

Agriculture rarely rewards a straight-line strategy. Markets swing with weather, commodity cycles, and shifting policy winds. At Ag Startup Engine (ASE), we’ve learned to treat liquidity the same way a grower treats harvest: you pick when the crop is ready, not when the calendar says so.

Earlier this year we were presented with the opportunity to participate in a secondary position in one of our top-performing portfolio companies. It was a deliberate move, not to cash out or hedge our bets, but to turn hard-won paper gains into real dollars.

As fund managers, our north star is simple: return capital to our investors. We do that by backing great companies. We don’t win by having the most assets under management. So when we can seize rare opportunities to turn markups into distributions, we should.

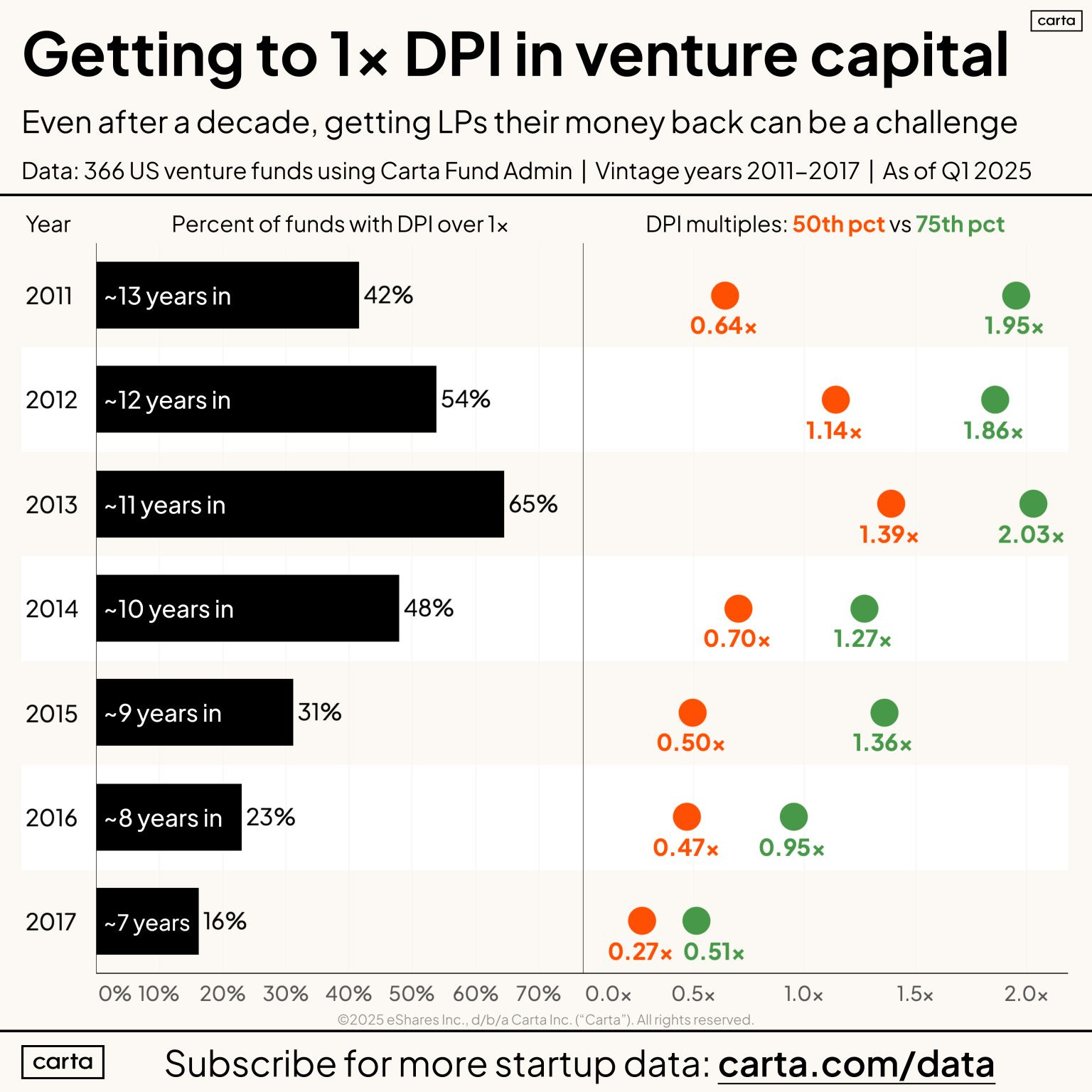

Because in today’s venture environment, realized returns feel like the exception…not the rule. And while the chart from Carta below reflects a subset of funds across all sectors, it’s fair to assume the numbers are even more sobering for ag-tech funds.

When even the best funds, 10+ years in, are barely hovering above 1× DPI, we have to ask ourselves:

How do we get real capital back to LPs in a market that offers so few opportunities to do so?

In this environment, markups aren’t enough. LPs don’t commit to the next fund on potential. They re-up when they get money back.

So here’s our thought process behind taking secondaries, and why, in ag markets especially, they aren’t and shouldn’t be a red flag. They’re a tool for disciplined, long-term investing.

1. Timing Matters. Especially in Ag

Exits in AgTech trail commodity and macro cycles. Capital floods in when climate headlines spike or food-security fears rise, then ebbs just as quickly. Those narrow windows create rare moments of dislocation, where demand and pricing surge, even if M&A activity remains sluggish.

One of our pre-seed bet was on a rocket ship. Top-tier funds were suddenly knocking on their door pre-empting a Series A fundraise and hungry for any room on the cap table. In AgTech, that kind of inbound interest is like a three-day stretch of perfect weather: you drop everything and combine while the grain is dry.

It was, in our view, a rare moment: liquidity in ag doesn’t come often, and it doesn’t come back quickly. You don’t fight seasonality in agriculture. You time your harvest.

2. Fund Construction in a Tough Market

Returning Capital, Not Just Rebalancing

ASE runs intentionally small funds. We back practical, capital-efficient ag businesses that can plausibly return 2–5x outcomes. We don’t need every company to be moon-shot unicorns (and most aren’t - see my previous thoughts about the $1B agtech lie). In today’s market, IPOs are unicorn-rare and M&A is whisper-quiet. LPs value cash more than fresh mark-ups.

So when liquidity knocked, the question wasn’t “Should we de-risk?” It was:

“Can we return capital to the people who trusted us, right now, when the broader ag market isn’t delivering many wins?”

We took capital off the table, locking in a realized return for our investors and showed that even in a down-cycle we can still send real checks home, not just stories, logos, or lofty projections.

It wasn’t about playing defense. It was about doing what we promised to do from the beginning: turn early-stage conviction into real, tangible outcomes.

3. DPI Beats TVPI (Every Time)

A glossy 3x TVPI is fine on paper, but LPs re-up on DPI. Converting a big paper gain into distributions turned abstract upside into hard evidence:

ASE can harvest value, even when traditional exits are stalled.

We’ve always believed that part of our job is not just finding the next great founder or supporting pre-Seed to Series A, but turning wins into distributions that justify the risk we took in the first place.

That credibility matters far more to our partners, many of whom come from farming and ag-business households, than another headline valuation.

**TVPI includes unrealized gains (or paper markups) on active investments. It reflects the total value on paper of a fund, blending what’s been returned with what’s theoretically worth more today.

In simple terms: TVPI = real dollars + Monopoly money. DPI = just real dollars.

4. Secondaries Are Discipline, Not Doubt

There’s a myth in venture that if an investor sells, it means they’ve lost belief.

In fact, freeing up that capital let us double down out of our next fund. We re-invested in the company:

We kept meaningful ownership.

The founders got continued support.

Our new fund captured fresh upside without over-exposing the old one.

That’s not stepping back, it’s a strategic reload.

In this case, secondaries weren’t about taking chips off the table. They were about making sure we had more chips to play the next round.

5. The Ag Startup Engine View

If you’re investing in agriculture, you already know that capital stacks are thin, timelines are long, and liquidity is anything but predictable. That’s why timing matters more here than anywhere else.

Great outcomes come from disciplined ownership, thoughtful timing, and staying grounded in market reality. Taking secondaries was one of the most strategic decisions we’ve made, and one we’d make again if the dynamics lined up the same way.

Because in this market, exits don’t come on a schedule and venture isn’t built on monopoly money. We’ll continue to treat secondaries as a tool for disciplined, long-term investing in the agricultural sector.